Quant Resume Buildings

- Quant firms들의 JD들에 대부분 partial differential equation (PDE)가 들어가 있음.

- Database 경험이 중요함: SQL

- All-in-one: Online webapp, hosted on my website.

- from free data sources:

- Daily pull of equity/ future prices.

- store in database, cloud hosted

- from free data sources:

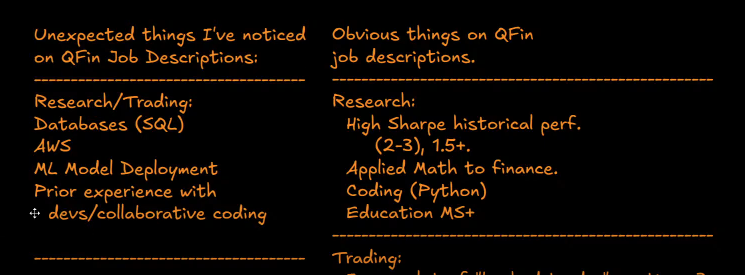

- Unexpected Things I’ve noticed on QFin JDs

- Research/Trading

- Database(SQL)

- AWS

- ML model deployment.

- Prior experience with Devs/Collaboration Coding

- Obvious things on QFin JDs

- High Sharpe historical performance.

- 2-3, 1.5+

- Applied Math to finance.

- Education MS +

- Coding: Python

- Pseudo IQ test: Wonderlic Test

- Options/Equity Market Making OR statarb

- High Sharpe historical performance.

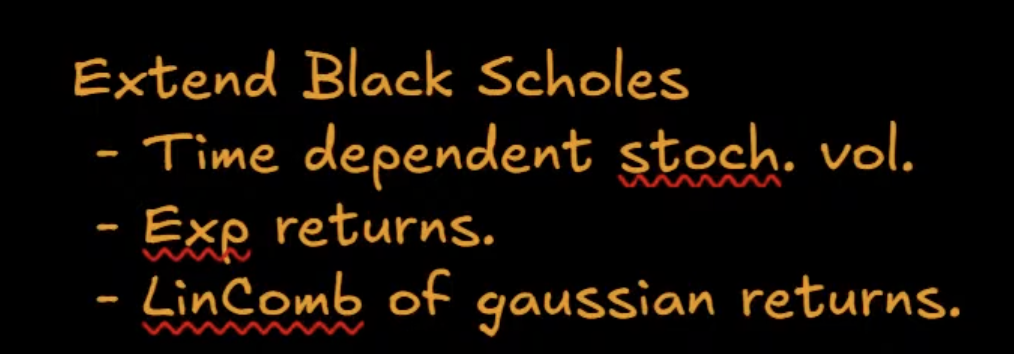

Mathematical Finance

Black Scholes

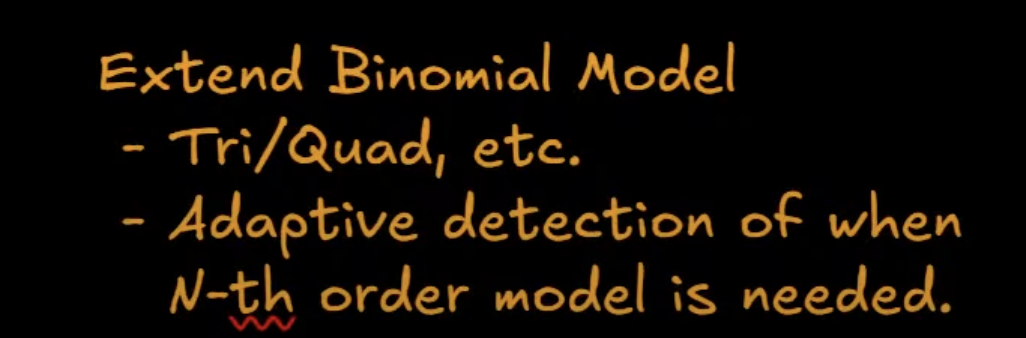

Binomial Model: Dai, T. S., & Lyuu, Y. D. (2010). The bino-trinomial tree: A simple model for efficient and accurate option pricing. Journal of Derivatives, 17(4), 7.

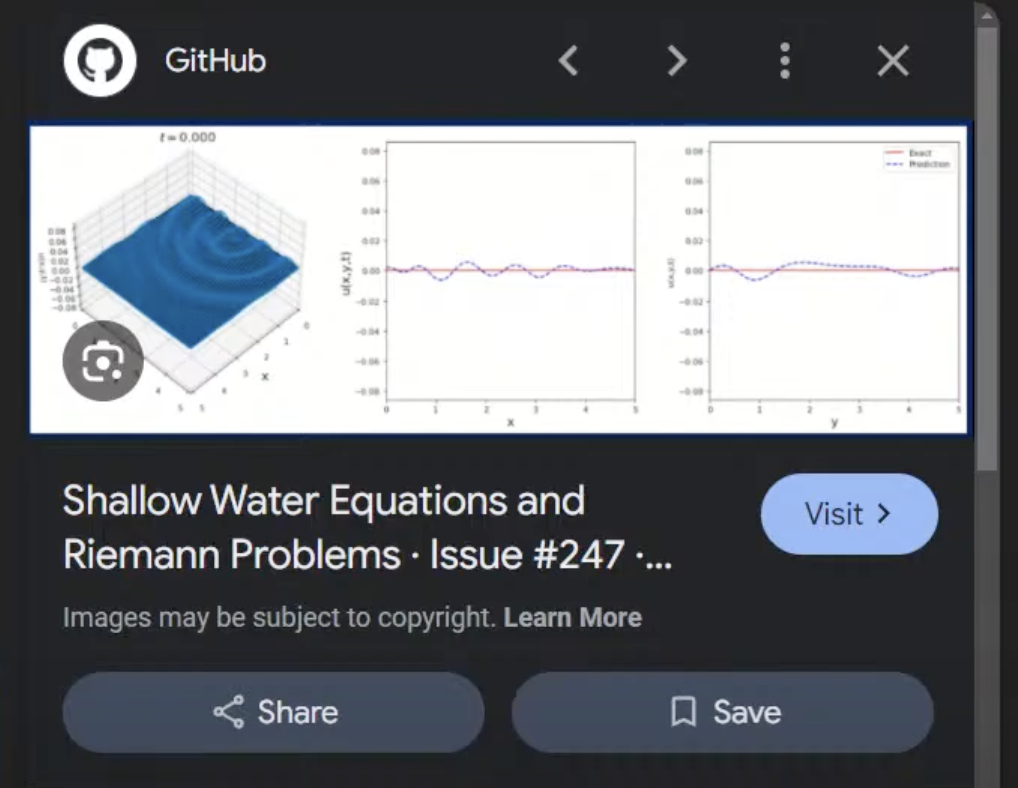

shallow water equation: https://users.oden.utexas.edu/~arbogast/cam397/dawson_v2.pdf

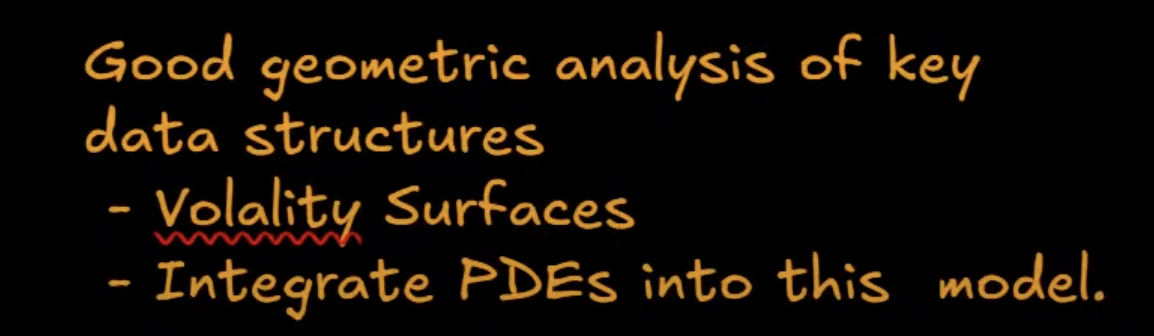

example image

Read Book

- Options futures and other derivatives

- statistical arbitrage review(최신걸로 읽기, google scholar)